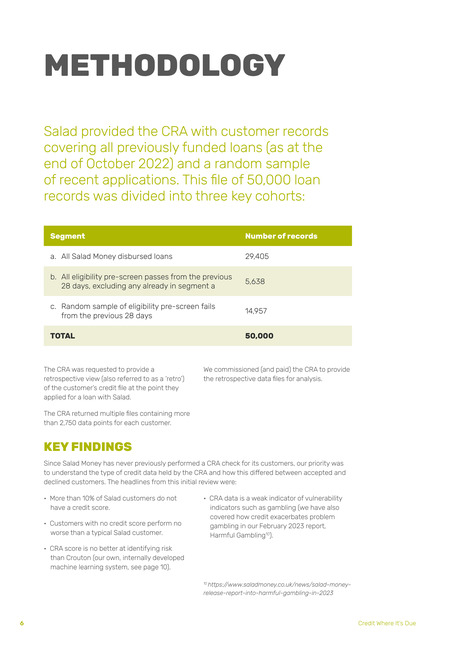

METHODOLOGYSalad provided the CRA with customer recordscovering all previously funded loans (as at theend of October 2022) and a random sampleof recent applications. This file of 50,000 loanrecords was divided into three key cohorts:SegmentNumber of recordsa. All Salad Money disbursed loans29,405b. All eligibility pre-screen passes from the previous28 days, excluding any already in segment a5,638c. Random sample of eligibility pre-screen failsfrom the previous 28 days14,957TOTAL50,000The CRA was requested to provide aretrospective view (also referred to as a ‘retro’)of the customer’s credit file at the point theyapplied for a loan with Salad.We commissioned (and paid) the CRA to providethe retrospective data files for analysis.The CRA returned multiple files containing morethan 2,750 data points for each customer.KEY FINDINGSSince Salad Money has never previously performed a CRA check for its customers, our priority wasto understand the type of credit data held by the CRA and how this differed between accepted anddeclined customers. The headlines from this initial review were:• More than 10% of Salad customers do nothave a credit score.• Customers with no credit score perform noworse than a typical Salad customer.• CRA data is a weak indicator of vulnerabilityindicators such as gambling (we have alsocovered how credit exacerbates problemgambling in our February 2023 report,Harmful Gambling10).• CRA score is no better at identifying riskthan Crouton (our own, internally developedmachine learning system, see page 10).10https://www.saladmoney.co.uk/news/salad-moneyrelease-report-into-harmful-gambling-in-20236Credit Where It’s Due

It seems that your browser's pop-up blocker has prevented us from opening a new window/tab. Please click the button below to open the link manually.