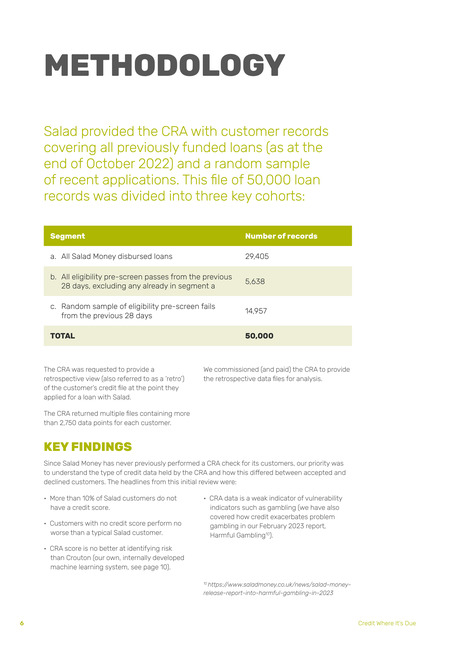

WHY WE UNDERTOOKA RETROSPECTIVEANALYSISChallenged ‘what value would CRA data have,over and above that of Open Banking?’ weinvestigated – and were shockedSalad Money is a social enterprisespecialising in affordable creditfor NHS and public sector workers.Salad launched in 2019 to addressa severe lack of affordable creditfor people with impaired, poor orthin credit scores and the millionsof credit invisibles. Our mission isto develop a sustainable mid-costcredit market and give borrowersan alternative to high-cost lending.We lend up to £1,500 over 12to 24 months. To do so we useOpen Banking data and our ownproprietary credit decisioningsoftware for affordabilityassessments, rather than creditscoring.Open Banking gives us visibilityof all key determinants for acomprehensive assessment ofcreditworthiness and affordability,including income from employmentand from benefit payments; allcurrent credit repayment liabilities;regular non-discretionary expensessuch as housing, utilities andgroceries; current and historicdifficulties with credit; signs offinancial stress and signs ofvulnerability. We see at least twelvemonths of data so we can assessapplicants’ financial trajectory andany changes.To date, we have lent more than £4mto more than 3,100 customers with nocredit score and who would otherwisebe excluded by lenders which rely onCRA data (we’ve lent more than £40mthrough over 46,000 loans in total,to more than 13,000 NHS employeesand over 18,000 other key workers inthe public sector).We have saved customers (46%of whom have children in theirhouseholds) millions of pounds ininterest compared with borrowingfrom the only alternative providersavailable to them.Beyond lending, Salad’s free financialsupport tool, Salad Money Mind, helpsSalad applicants (not only customers)build financial resilience.As part of this review, Saladattempted to address threekey areas:1. What can CRA data tell usabout our customers thatwe don’t already know?2. What impact wouldCRA data have on ourunderwriting process?3. Would CRA data improveour decision-makingcapability sufficiently tojustify using it?Our retrospective analysiscovered 50,000 loan recordsas described on page 6.In 2022, Salad was challenged tounderstand what value CRA datawould have, over and above that ofOpen Banking. Salad engaged withone of the UK’s three main creditreference agencies to complete aretrospective analytical exercise,which would provide Salad with acopy of the customer’s credit file atthe point they applied for a loan.Comparing the value of Credit Reference Agency data with Open Banking when serving financially excluded people5

It seems that your browser's pop-up blocker has prevented us from opening a new window/tab. Please click the button below to open the link manually.